GHAPS Asks Taxpayers for Unlimited NON-QUALIFIED Bonds

When asking taxpayers to approve new bonds, school districts have three main options: qualified, non-qualified, and sinking funds. In May 2023 when GHAPS asked taxpayers for $155 million to build a new school, new multi-purpose building and list of other items, GHAPS chose the QUALIFIED option. GHAPS has since split the May bond proposal into two separate proposals that total $146 million and will ask voters for approval in November 2023, but this time they have chosen the NON-QUALIFIED option. Why?

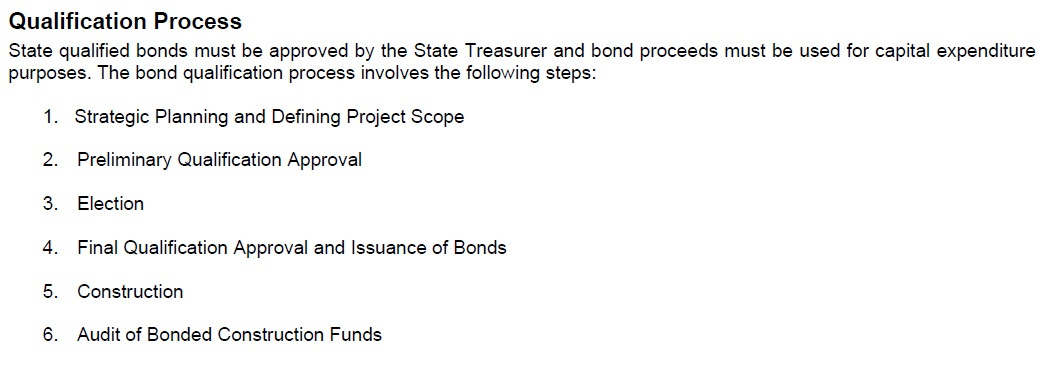

The state bond qualification process is overseen by the State of Michigan, and the final step is an audit of the bond funds. It appears that the non-qualified bond option does not require an audit, and there is no government oversight. Is it really possible that GHAPS is asking voters for an audit-free $146 million bond even after the recent $1+ million embezzlement? Are they serious?

To answer these questions, it is important to understand a few key differences between the options. According to Wolgast Corporation, a construction company that does work for school districts, the non-qualified option is available to districts with good credit. "With good credit, the district doesn’t have to rely on the State to co-sign for the bond and [the non-qualified option] provides some more flexibility in the expenditure of funds. [] Additionally, through a Non-Qualified Bond Program, School Districts have the opportunity to shop for their own lender (either competitive or negotiated sale) and get a better interest rate, so they can do more with the monies their bond program generates."

In other words, school districts can avoid oversight and skip most of the paperwork process required by the State Treasury department, which can take over 12 months to complete, enabling them to complete the process in approximately 3 months.

According to the presentation attached below from PFM Financial Advisors LLC, non-qualified bonds have potentially higher millage rates, potentially higher borrowing costs, are not regulated by the state, and have less oversight.

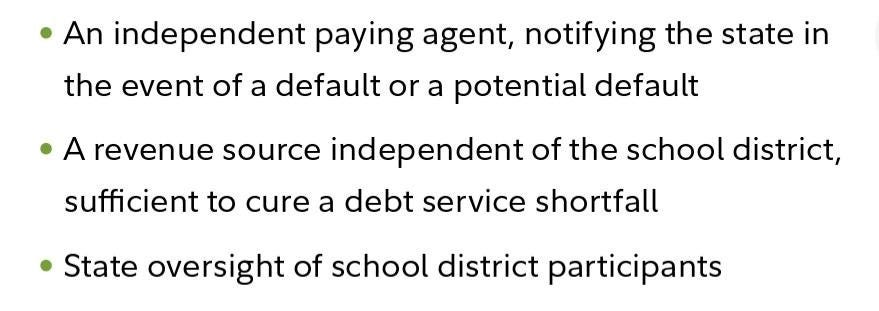

Conversely to non-qualified options, Fidelity Capital Markets explains that state qualified bond programs ensure these three things:

A mechanism in place to notify the state if a district is going to default.

The state is a co-signer to ensure the loan will be repaid.

The state provides oversight. (In Michigan state oversight is the audit).

As voters, we must be able to trust the district is acting in good faith. We have to be confident the district is financially secure to be able to repay the loan. We need to know bond funds will be spent responsibly and appropriately.

But currently GHAPS does not appear to have an accounting system in place to adequately track spending, and they have spent lots of money on billboards and perception management. How will a self-audit be handled?

The qualification process takes time and GHAPS did not have time for another qualified bond proposal to go on the November ballot. They are in a rush! These two non-qualified bond proposals are $9 million less, and are potentially riskier for taxpayers. Excluding an audit does not re-establish the trust that was lost from the embezzlement.

To quote the advice from King Media's post-election intelligence report which was financed by our community:

“The community clearly wants more conversation, evaluation of options, impact studies and plans for the existing site if a move is necessary. This process can’t feel rushed or superficial –it has to be thoughtful, genuine and intentional.”